What is Account?

Account is journal, ledger, cash book, book keeping, recording, of financial transaction. Account is also known as accounting or accounting system.

What is Accounting (Accounting System)?

- Accounting is the process of identifying financial transaction, systematic and scientific record keeping, classifying and summarizing and preparing final statement in order to provide financial information to the concern authorities.

- Accounting is language of business.

- Accounting is mirror of financial transactions.

- Accounting is art and science of book keeping and reporting process.

- Accounting is combination of records, reports, ledger and financial documents that are related to the legal transactions.

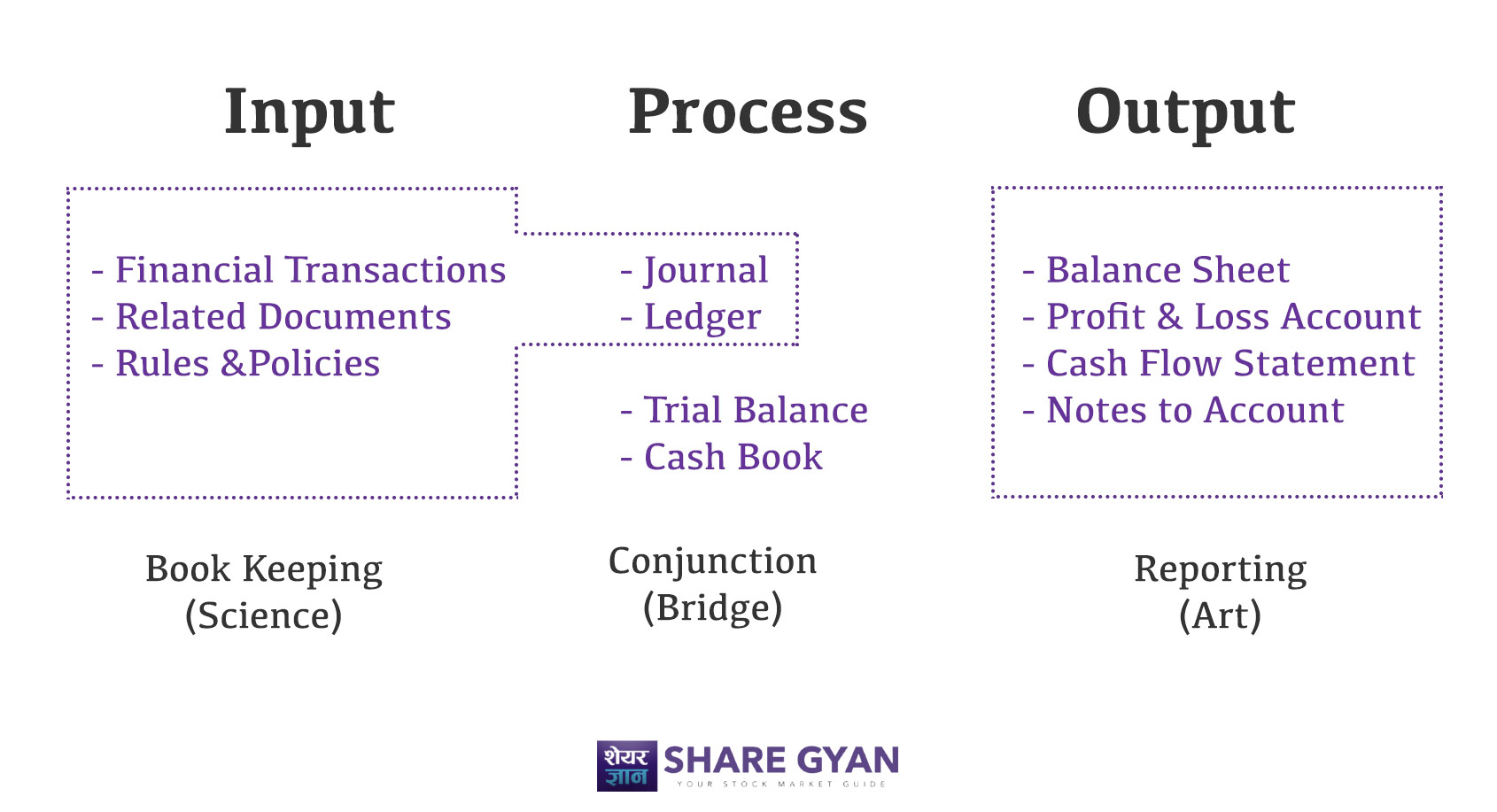

- As show in the diagram below, it consists of input, process and output.

Note – Trial Balance works as bridge between book keeping and reporting.

Functions/Objectives/Benefits of Accounting

- Identification, recording, classification, analyze, summarization of financial transaction.

- To present the true financial status of the organization.

- To show the performance of the organization.

- To present detailed financial transactions to stakeholders.

- To maintain the balance in financial transaction.

- To help management of financial transaction.

Bases of Accounting (System of Accounting) – लेखाको स्वरुप

- Accrual Basis Accounting (प्रोधभावी लेखाप्रणाली / वास्तविकतामा आधारित )

- Cash Basis Accounting – (नगदमा आधारित लेखाप्रणाली)

1) Accrual Basis Accounting

Accrual basis accounting system records all the transaction ignoring whether the cash is receipt in the transaction.

- Accrual basis accounting system records both cash and credit transactions.

- It also records past transaction and future transaction whether cash is receipt or not.

- It helps to prepare final accounting.

- It follows all the principles of accounting.

- It records the depreciation as well.

Advantages

- It follows all the accounting principles.

- It records both cash and credit transactions.

- It helps to forecast.

- It records depreciation.

- It helps to prepare final account.

Disadvantages

- Expensive

- Needs skilled manpower to prepare.

- Complex system.

- Not suitable for all types of organizations.

2) Cash Basis Accounting

In cash basis accounting, the a counting record is recorded based on the cash inflow and cash outflow. It consider only cash transaction.

- It is simple and straight forward accounting.

- No record of credit transaction.

- No record of depreciation.

- Cash basis accounting does not follow all the principles of accounting.

- It controls the bash transactions.

- Based on the double entry system however, we can also record as per the single entry system.

- Cash basis is used in the government firms.

Advantages

- Easy and simple.

- Both single entry and double entry can be used.

- It controls the cash.

Disadvantages

- It does not show the true state of transaction.

- It does not follow all the principles of accounting.

- It ignores depreciation.

- It is not suitable for all the organizations.

Note – Comparing these two accounting systems, accrual basis accounting system is best because of the above mentions reasons. Banks and Financial institutions use accrual basis accounting system.

Types of Account/Accounting

There are many ways we can keep accounting. Different organization implement different accounting system as per their nature.

- Single entry accounting

- Double entry accounting

- Cash basis accounting

- Accrual basis accounting

- Banking accounting

- Management accounting

- Financial accounting

- Non-governmental accounting (non-financial)

- Lean Accounting

Principles of Accounting

Accounting principles are those which are accepted and adopted while developing the accounting. These principles are also called Generally Accepted Accounting Principle (GAAP).

- Money measurement concept – Only monetary transaction which can be expressed in monetary value are recorded in accounting but non monetary transactions are not recorded in accounting.

- Business entity concept – Business and owner must be treated separately. Business entity concept defines that the transaction between business entity and business owner must be recorded separately.

- Accrual basis concept – Accrual basis defines that record all the business transactions including cash, receivables and payable transactions. All the transactions that carried out on a given period of time should be recorded in accounting regardless of payment made.

- Cash basis concept – Accounting keeps record of only cash based transactions of a certain period of time. This is just an opposite of accrual basis concept because it excludes receivables, payables.

- Single entry concept – If there is no rule of debit and credit while recording in accounting the this concept is single entry concept. This concept is only used in household sector but not used in business and organization sector.

- Double entry concept – In double entry concept, every financial activities are recorded by using the rule of debit and credit. Double entry system is fundamental, modern, scientific, systematic and widely adopted concept of accounting.

- Going concern concept – Organization will run forever. Going concern concept considers that any organization will run forever regardless of its owners. So, while performing accounting activities, it should be considered that organization will run forever.

- Matching concept – There must be coordination between income and expenses of the entity. Those expenses related to income generation within a given period of time must be recoded in the same title. This concept defines that if you invest, you should get a return. Depreciation is recorded with this concept.

- Historical cost concept (cost concept) – Organization record financial transaction considering the original price not market price. The valuation of fixed assets must be recorded in its original price not it current market price.

- Accounting period concept – Accounting period considers every 12 months as accounting period or fiscal period. It is also called periodicity concept.

- Realization concept – This concept defines that accounting should be recorded only after financial transaction is happened not in the possibility of the event.

Besides these principles, there are other traditions regarding the accounting process. They are

- Conservatism – संकुचनकारी सोच

- Consistency – एकरुपता

- Full disclosure – पूर्ण पारदर्शिता

- Materiality – औचित्यता

Other Posts

- BAFIA 2073 Major Highlights

- Company Act Highlights – Banking Notes

- ADBL – Establishment, Development, Work Nature, Mission, Vision & Objectives

- What is KYC (Know Your Customer) in Banking?