What is lending?

Lending is the process of advancement of the amount to the individual or institution.Lending, borrowing, overdraft are the same concepts. It can be short-term and long-term. Lending is the core function or fundamental function of banks and financial institutions.

Banks and financial institutions by charging a fixed amount of interest, such interest income is a major source of income. A person who takes a loan is called a loanee or borrower. Providing credit is a dominant asset of banks. For a bank, 20 to 25 % of income comes from other sources whereas 75-80 % of income comes from interest income.

The interest rate & time period is fixed before advancing the loan to a borrower. A borrower has to accept the terms & conditions imposed by the lender.

Types of lending

| Base | Type |

|---|---|

| Tenure | 1) Short Term Loan – repayment period of less than 1 year 2) Mid Term Loan – Not in practice 3) Long Term Loan – repayment period of more than 1 year |

| Security | 1) Secured Loan – Loan with enough collateral securities 2) Unsecured Loan – Loan is given without enough collateral securities |

| Customer | 1) Individual Load – Loan provided to the individual person i.e. natural person 2) Institutional Loan -Loan provided to the artificial person, legal person i.e. organizations. |

| Modality | 1) Single Bank Loan – Loan provided by the single bank only 2) Consortium/ Syndicate Loan – loan provided by more than one bank |

| Treatment | 1) Funded Loan – In funded loan cash outflow from the bank 2) Non-funded Facilities |

| Nature | 1)Term Loan 2) Working Capital Loan 3) Consumer Loan |

What is a Non-funded Loan?

Non-funded facilities are those facilities where the bank’s funds are not involved. The bank provides its services as an agent of its customer. For example bank guarantees like performance guarantees, bid bonds, deposit guaranty, financial guarantees, money retention guarantees, advance mobilization guarantees, letters of credit (LC), etc.

What is Term Loan?

A term loan is a type of loan that is provided with sole purpose of creating fixed assets, incorporation of a firm, development, and expansion of industries. A term loan is generally for more than one year and can not be renewed. In term loan, there is fixed predefined installment amount to be repaid within the predefined period. Term nature loan can not be renewed but can be restructured and rescheduled as per the guidelines and directive from the central bank.

What is Working Capital Loan?

The working capital loan is provided for the day-to-day operation and generally be of a short period of time (less than 1 year). The duration may be longer if the working capital gestation period is longer. This loan is provided for day-to-day operations. There is no fixed installment amount to be repaid in regular basis but interest should be repaid to bank in quarterly or semi annually or annually basis as per the agreement between the bank and borrower.

Working capital loan can be renewed before it expires. In Nepal, all Bank and Financial Institutions must follow the Working Capital Loan Guidelines by Nepal Ratra Bank while providing working capital loan. (नेपालमा बैंक तथा वित्तीय संस्थाले नेपाल राष्ट्र बैंकको चालु पुँजी कर्जासम्बन्धी मार्गदर्शन, २०७९ को अधिनमा रहेर चालु पुँजी प्रकृतिको कर्जा प्रवाह गर्नु पर्दछ)

Major Differences between Working Capital Loan and Term Loan

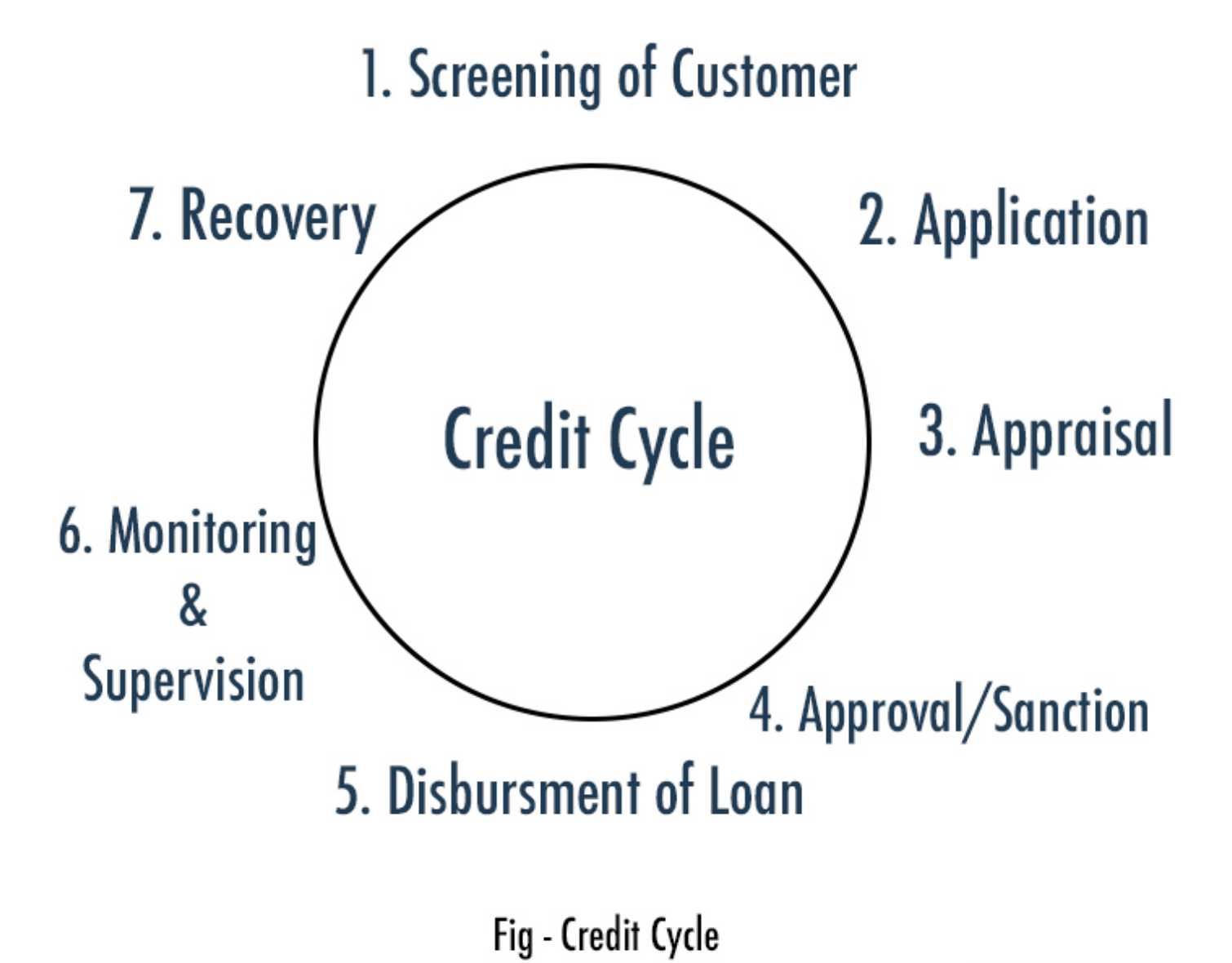

What is Loan Cycle | Credit Cycle | Lending Cycle?

There are 7 steps involved in the lending cycle they are presented in the fig. as below.

Appraisal (कर्जा दिनु भन्दा अगाडी बैंकले गर्ने मुल्यांकन)

- Appraisal for Consumer Loan

- Appraisal for Project Loan

For Consumer Loan (7 Cs of Credit | 7 Cs of Lending )

Following are the 7 Cs that must be considered while lending by banks and financial institutions to a consumer loan.

- Character – how mus is the borrower willing to pay back?

- Collateral – pledge by the borrower to secure the loan

- Condition – what are the conditions for providing credit. If the loan is needed for setting up a retail business in a particular area, then the lender must take a thorough study of the economic conditions.

- Credibility – how credible is the borrower

- Capacity – sources of repayment

- Credit terms/policy/standard – what are the terms and conditions. It should not go against the policy

- Capital – financial conditions of the capital structure. Eg. the debt to equity ratio, current ratio, interest coverage ratio, debt to assets ratio, etc.

For Project Loan

Different aspects are analyzed while conducting an appraisal for a project loan. They involve-

- Technical Aspect

- Financial Aspect

- Management Aspect

- Marketing Aspect

- Legal Aspect

- Socio-environment Aspect

- Securities Aspect

- Environmental Aspect

- Analysis of Collateral etc.

Principles of Lending

We provide the loan to customers by considering the following principles.

- Principle of liquidity – make sure there is enough liquid fund

- Principle of safety – make sure investment is safe

- Principle of profitability – focus on making a profit while lending

- Principle of diversification – concept of “Do not put all the eggs in one bucket”

- Principle of social responsibility – social responsibility should also be considered

- Principle of national interest – consider national interest while lending

- Principle of objective – invest in those projects or that customer who has got objective

Other Posts

- What is KYC (Know Your Customer) in Banking?

- RBB 4th & 5th Old Question Paper Collection

- What is Deposit and its Types